You return from school one afternoon, open the mailbox in your apartment building in western Massachusetts, and pull out a thick envelope. Heart quickening and hands shaking, you tear into the envelope of your first-choice school—Merrimack College—and you read the first line, “Congratulations and welcome…”

Last week, you were accepted to Pace University and your local public university, Fitchburg State. You immediately call your mom and celebrate on the phone. It is a thrilling moment and a testament to all your hard work, and to your mom’s hard work as a single parent.

Now a new waiting game begins. You need to figure out how much each option will cost. You know college is an investment in your future, but how much of an investment can you afford? Cost is the primary factor you and your mom will use to determine where you attend college next year.

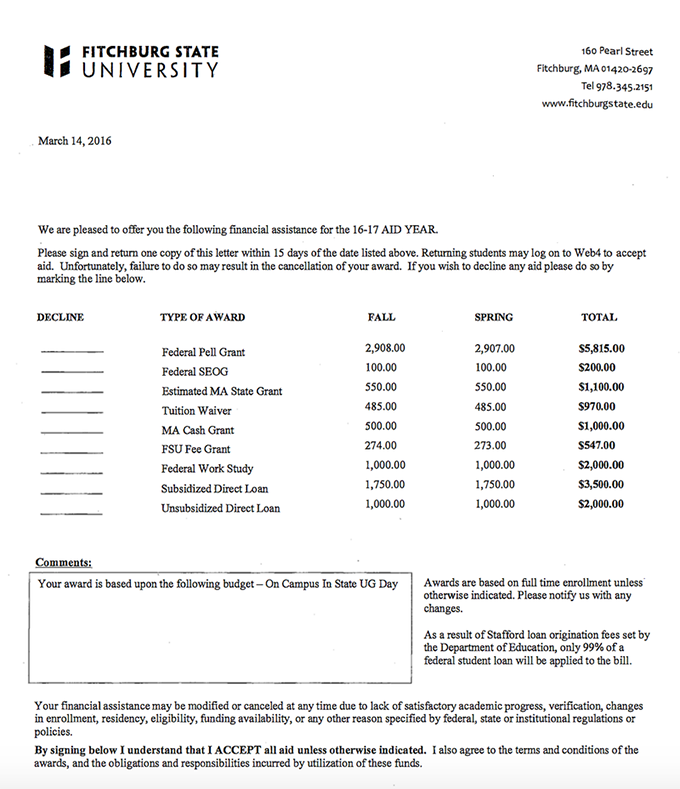

A couple of weeks later, you receive your first financial aid package, from Fitchburg State. You scan the information and confusion creeps in. You look for the bottom line: what is this going to cost? It does not seem to say anywhere. As you go through the list of financial aid “awards,” you notice there are two loans. A loan does not feel like an award at all.

The good news is that you received four grants, money your guidance counselor tells you will not need to be paid back. But there are a few terms you have never seen before. What exactly is “Federal SEOG,” “Tuition Waiver,” and “Federal Work Study”? Clearly, you will have to do more research to figure out exactly how much you would need to budget for Fitchburg. The first step will be trying to track down how much it costs. Then maybe your counselor can help you figure out what you would need to pay or borrow. Maybe she can explain all those other things listed.

Three days later, you receive the financial aid package from Merrimack. It looks totally different from the one you received from Fitchburg, making it difficult to compare the two. Your heart lifts as you see that you have received a large scholarship.

As you move through the letter, though, your heart sinks. Merrimack is very expensive. Tuition and fees and room and board alone are over $53,000. After subtracting all the aid, some of which are loans, it looks like there will still be $19,955 left to cover. Merrimack lists different ways to pay that remainder, but the terms listed are unfamiliar. Merrimack mentions you could earn $1,500 in “federal work study” or “Merrimack work.” This aid could help you cover a small fraction of your costs, but it is unclear if you qualify and if it is one job or two.

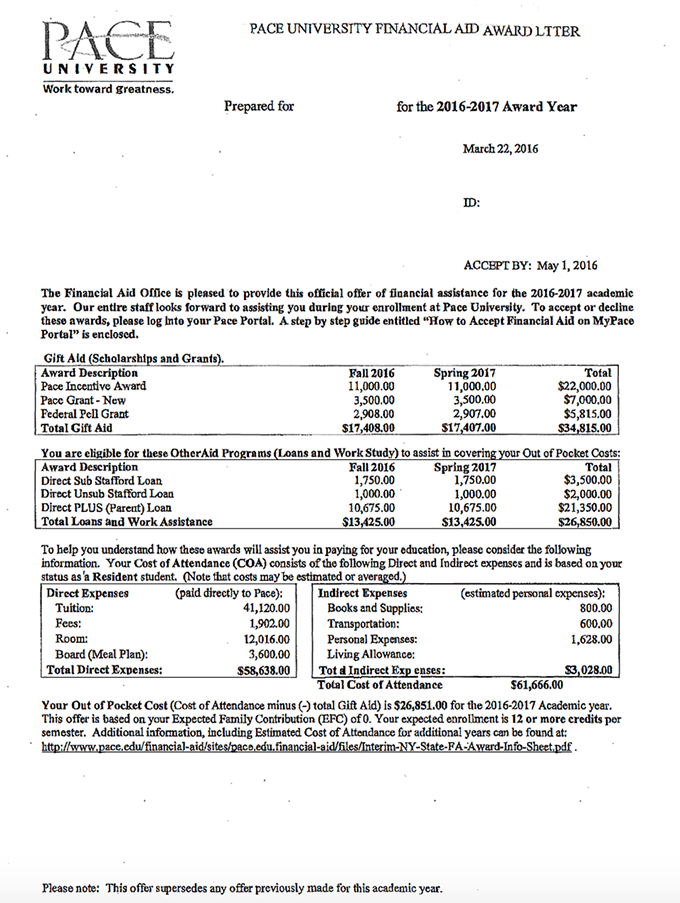

A few days later, you receive your last award letter, from Pace University in New York. You feel like you know what to expect now with these letters, but Pace’s looks completely different than the other two and includes even more information.

At least Pace separates “gift” aid from loans and work-study so you can see this is your biggest gift aid offer yet, with nearly $35,000 in grants and scholarships. But Pace also costs more, at $61,666. Unlike Merrimack, though, Pace lists more costs than tuition and fees and room and board. Pace includes other expenses like transportation, books, and supplies, expenses you had not really thought about until now. You see that a new loan is mentioned in this award letter, the “Direct PLUS (Parent) loan,” for over $20,000. Would Mom have to borrow the money since it says parent? Mom only makes $35,000 as a paralegal, so a loan that high is not an option, especially given that your younger brother wants to go to college, too.

The excitement of choosing your college fades as confusion about what each school costs and how your family will afford it sets in. Maybe college isn’t for you after all.

Millions of prospective students nationwide face scenarios just like this one. Why are financial aid award letters so difficult for students and families to decipher?

No federal policy exists that requires standardized terminology, consistent formatting, or critical information on every financial aid award letter. Without guidelines, like federally-required nutrition labels or the window sticker for car sales, the consumer is left without an apples-to-apples comparison for a major financial decision. The lack of required elements leaves thousands of institutions communicating about billions of dollars of federally-funded aid in hundreds of different ways. Many use the same term in different ways, some with costs missing, and others lumping all grant and loan aid together. This current hodgepodge approach does not work. It puts both today’s students and our nation’s investment in higher education at risk.

Poor communication of financial aid options can threaten the student’s (and sometimes her parent’s) long-term financial health by obscuring the basic terms and conditions of aid. Financial decisions based on incomplete and incoherent information place students at risk of facing unanticipated costs. Worse yet, obscuring costs puts students at risk of dropping out if their bill is bigger than anticipated—and dropping out is one of the major predictors of federal student loan default.

Award letter components must be standardized to give students and families the critical consumer information they need. For this reason, New America’s Education Policy Program partnered with uAspire, a nonprofit leader on college affordability, to analyze data from thousands of financial aid award letters.

In Decoding the Cost of College: The Case for Transparent Financial Aid Award Letters, we provide background and context for this work and show infrequently need is met for low-income students. We explore a data set of hundreds of unique award letters to illustrate the many different ways colleges and universities communicate college costs and aid. We provide recommendations for policymakers and practitioners to improve financial aid award letters so that they are student-focused and drive better-informed decision-making.

Download the full report here.